big pile of overlapping credit cards covering surface

What is Debt Consolidation (DC)? Should you consolidate?

Times are tough overall, and for some, things are just dire. Many families have recurred to credit cards to make ends meet. I have had several clients asked me what I think of Debt Consolidation? Should they consider it? Will it helped them get their debt in check? Will they be able to purchase a home sooner?

To begin, lets define DEBT CONSOLIDATION (DC)

The gathering of all debts into one large sum to be paid in prescribed monthly terms, with a fixed interest rate for a specific period. Most of the times, the consolidated loan is paid off in 5 or 10 years.

Should you consider it?

Yes, you lose nothing by trying. However, be aware that not all unsecured debt can be consolidated. The companies that provide these services must reach out to your debtors and negotiate on your behalf. Some vendors may allow you to consolidate your debt but may place you on a “blacklist” for several years preventing you from attaining credit with them for an exceptionally long time. Each credit card (main providers of unsecured debt) has its own process of handling debt consolidation, and if you happen to have more than one type of credit card with a said vendor, one line of credit may be approved for the consolidation while the other is not. Before committing to a consolidation program, do your homework. Talk to more than one provider. DON’T LET THEM RUN YOUR CREDIT or HAVE ACCESS TO YOUR LINES OF CREDIT. (Go to https://www.virginiadebtrelief.org/) for more information on the local Virginia program.

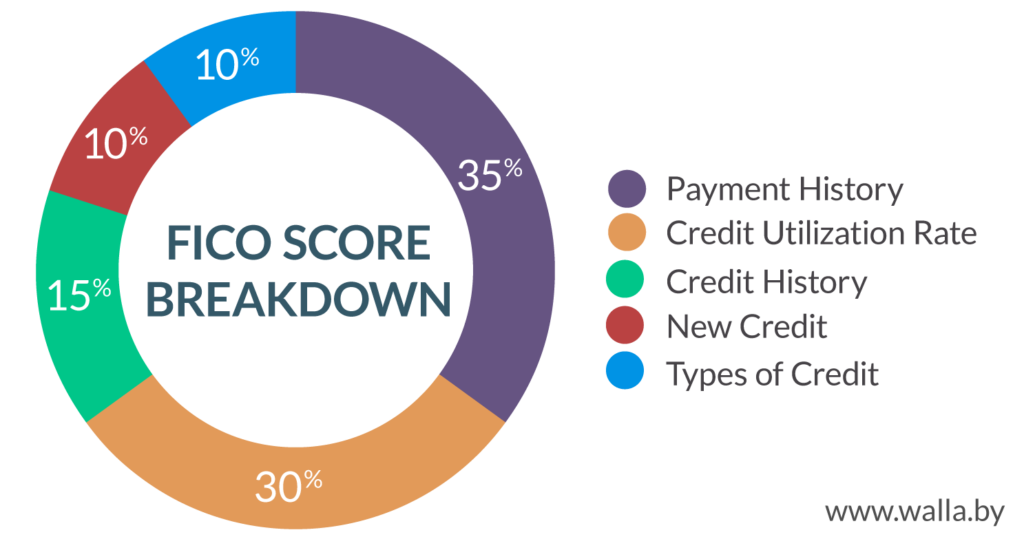

BE AWARE that going through a consolidation process, will have a NEGATIVE effect on your credit history and credit score; sometimes more deterrent than not going through the consolidation process itself. When a vendor allows your line of credit to be consolidated, that line of credit is closed. You are responsible for the debt but no longer have access to any line of credit previously available. Closing lines of credit wipes away any history of the credit you ever had. Once the line of credit is closed, it cannot be recovered.

Are there other options?

Yes. There are other options to consider before consolidating. Here are some suggestions.

- Draft a letter to each creditor, and directly plead your case. Be precise. Request an adjustment in the interest rate and/or minimum payment. Review the length of time you have been a consumer with them and the exemplary record you have with them. You lose NOTHING by TRYING.

- Secure an additional source of income and apply the new income to paying debt off. Even a minimal amount will make the difference. You, more likely did not accumulate all your debt in one step, so one step at a time, tackle that debt.

- List all debt from smallest to largest amounts and tackle the debt from the smallest amount largest. Dave Ramsey® is a person that I follow extensively for financial advice. He calls this step the SNOWBALL effect. He recommends you focus on the amounts of debt, not the interest rate. By paying off an account, it helps you emotionally to continue to fight for your financial freedom. You gradually go up the ladder of debt until you reach that solvency period.

- Set up a budget and stick to it. A budget should not be a word to fear nor is it meant to enslave you. A budget is a tool that can program your income to specific tasks at a precise time, so you are in control of your assets. Your salary is yours; you should manage it/direct it not the other way around. As you set up a budget and track your expenses, you will be realized right away where some points of stress are and where some points of mismanagement are. (These two are not the same thing). Don’t be intimidated by a budget. A budget is a ROAD MAP for your money. (Go to https://www.daveramsey.com/dave-ramsey-7-baby-steps/)

Should you consolidate?

I cannot answer that question for you as I do not know the full picture of your financial profile and financial goals. A debt consolidation will be recorded in your credit history and it will have an impact. The effect of it, may not be as detrimental as you completely failing to pay your debts. Some families have opted to file for bankruptcy versus doing a debt consolidation. This step is a whole new ball game and there are many questions that need to be asked, researched and answered about it. Not everyone qualifies for debt consolidation and/or for bankruptcy. Before taking this step, I suggest you draft a letter addressed to each credit vendor and try to reach an agreement with them.

I am no financial advisor, but I do have experience with debt consolation as a consumer. The first time I went through a debt consolidation was due to my credit card raising my APR three times the rate it had charged previously for several years. According to the credit card, I had made two late payments, thus they had the right to increase my interest rate. I had evidence that the payments had been made on time (direct deposit receipts). I made several attempts to get my interest adjusted, but the credit company refused. I spoke to my credit union, and they offered me an option to consolidate my debt. I did that and did not have any more dealings with this credit card.

The second time I went through debt consolidation was during and after my divorce. I needed to established credit on my own but also needed to restructure my financial responsibilities. I follow the steps of debt consolidation with 80% of my debt so I would not completely lose my lines of credit. Prior to signing the debt consolidation agreement, I reached out to each vendor in writing and personally informed them of the decision I felt I needed to make to assume my financial responsibility and stay afloat. Five of the credit vendors accepted my letter, my request to be consolidated, and did not blacklist me. I set my budget so I could pay off the debt consolidation in 4 years instead of 5. My credit score took a dip for about 6 months after the consolidation was set up, but then gradually began to rise. Within a few years of the consolidation, I was able to open a line of credit. After two years of the consolidation, I was able to buy a home. This was partly due to me keeping some lines of credit open, which had retained my credit history.

Resources to consider:

Money Matter by Dave Ramsey * Start Late, Finish Rich by David Bach * The Automatic Millionaire David Bach * Women & Money by Suzy Orman

#financialfreedom #debtconsolodation #paycreditcardsoff #budget

#beginthehomejourney #homebuyers #homesellers #paydebtoff #payprincipaloff #debtfree #luisahomejourney #homejourney #financialfreedom #principalpayoff

#homesforsale #realestateagent #sold #forsale #properties #mortgage #home #property