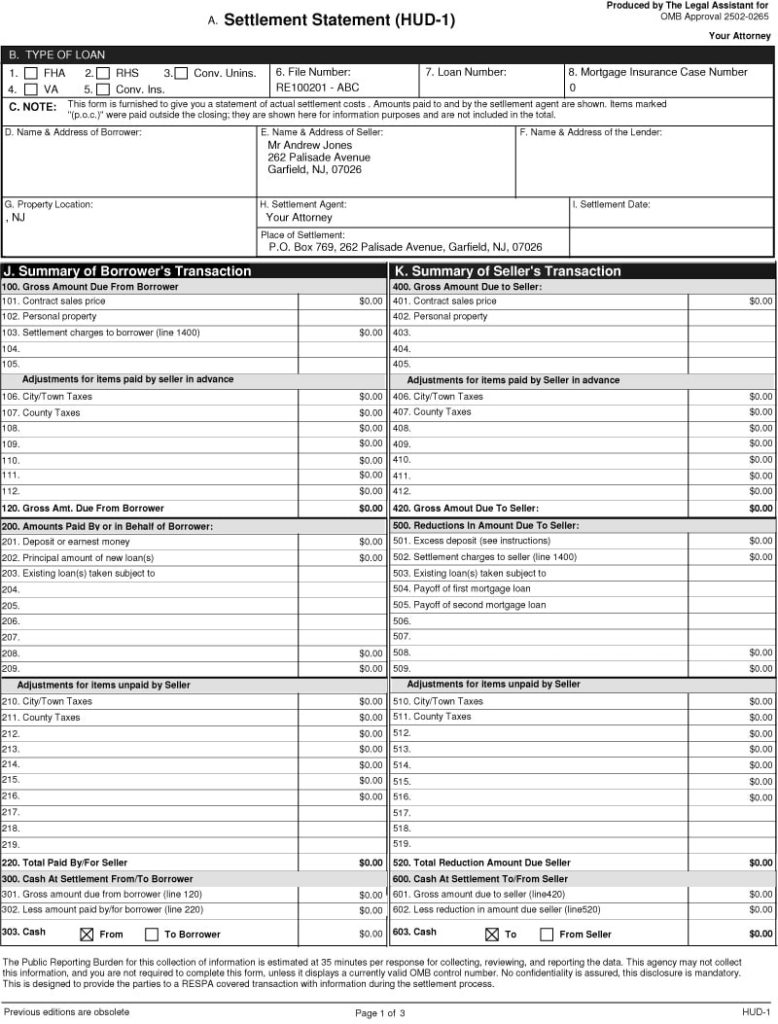

HUD-1’s & ALTA’s

Honey, let’s go buy us a house! It’ll have a backyard to host the summer’s BBQs, a sunroom for the cat to nap, a mancave to watch the game in, or maybe the pool we always wanted. YES! Let’s go buy ourselves a home! Congrats! This is the dream of every human and not just of Americans. Everyone wants a little piece of heaven to call home. However, the process can be a little daunting. A strong team comprised of a professional Realtor, a knowledgeable lender, a few licensed inspectors, and a reputable title company can guide both the buyer and seller through what can sometimes be a difficult transaction.

For sellers saying goodbye to a great neighborhood where the family has a plethora of anecdotes and memories of great neighborhood parties can be more stressful than other factors that must be assessed. Will they get the right price for their home? Will they find a great neighborhood to move into; would it be affordable? Will the new community be as appealing and family-friendly as their previous neighborhood? Will it have the same ambiance, historic and cultural markers as their current area does?

Buyers also have a boatload of anxiety about their future homes. Their loan portfolio and finances lead the way to many sleepless nights. Affordability aside, buyers also have to balance if they can afford it with is this right school, the right size home, how bad will the commute be, will the children fit in, will Fido run away? These and so many more emotions and decisions gradually have to be weighed in and resolved.

The house gets listed for sale, the buyers submit strong offers, an offer is selected; the inspections and appraisal all get ordered, conducted, and NEGOTIATED. Finally, the blessed day arrives when you get the CLEAR TO CLOSE. You breathe a sigh of relief. You have made it. No more sleepless nights! No more wondering of all the possible what-ifs scenarios that can derail all your hard work, and discipline.

It is done!

Time to rally the troops to finish packing and get to SETTLEMENT!!!!!!

Closing Disclosure

Yes, it is time for settlement! Well, it is almost time to settle….almost there. Right before you go to settlement, the buyer’s lender MUST give the buyer a very precise and well-prepared document called a CLOSING DISCLOSURE.

What is a Cloisng Disclosure?

The Closing Disclosure (CD) is a Five-page document given to the BUYER by the lender THREE days prior to going to settlement. IT MUST be given to the buyer. According to Consumer Financial Protection Bureau (CFPB), the CD statement will have the following details:

*Loan terms based on your loan type

*schedule of fees to buyer

*Schedule of costs to buyer

* projected mortgage

The CD is given to the buyer three days prior to settlement, to give the buyer time to evaluate the CD, the costs listed, compare it to the LOAN ESTIMATE initially given to them, and of course to have any lender questions answered before the final signature is recorded.

Upon reviewing the CD, the buyer(s) sign it, and three days later, the buyer and seller go to SETTLEMENT.

NOW, It’s Settlement time!

During the settlement, both buyers and sellers signed a plethora of papers. Emotions and nerves are still high. The final signature gets recorded and the Settlement wraps up. Sellers go off to get their move on to the next phase, to deposit their earnings, talk to their CPA, to celebrate, etc. The buyers also go off to celebrate, to move in, to set up last-minute utilities, to shop for new furniture, change their address, and maybe be get some sleep. Everyone is excited! Relieved! Emotions run high for different reasons now that it is easy to lose focus and misplace critical DOCUMENTS. The lack of focus can lead to a huge misstep that many a buyer and sellers have done.

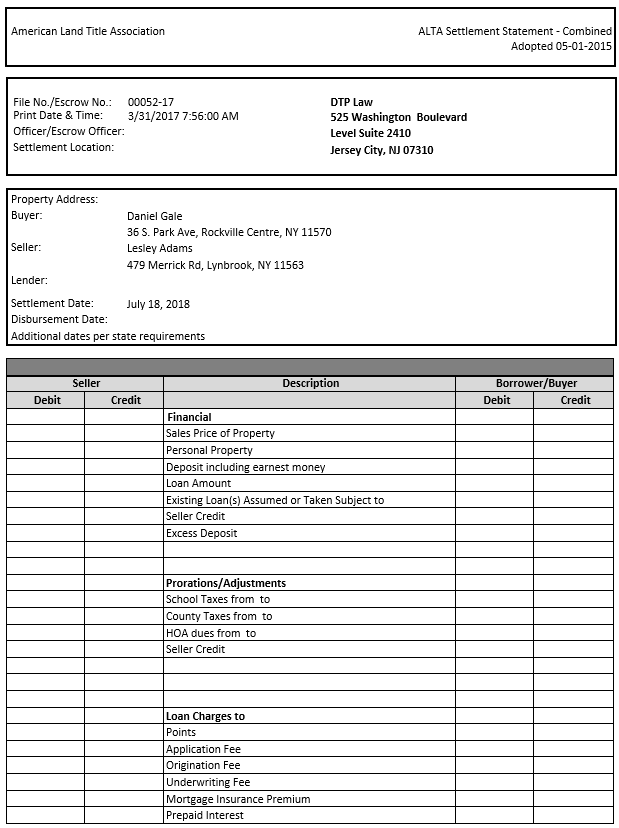

During the actual settlement, both buyers and sellers signed a document called an: ALTA Settlement Statement

What is an ALTA SETTLEMENT STATEMENT?

According to UpNest.com, the ALTA Settlement Statement is an itemized outline of all the costs each seller and buyer incurred in a real estate transaction. In addition, all credits and expenses associated with the transaction will be recorded in this document. All sellers and all buyers must sign this document. The ALTA Settlement Statement is the previous HUD-1 statement buyers and sellers received on a real estate transaction before October 2015

Upon ratifying all settlement documents, each party will receive a copy of the signed documents (receiving these documents may take a few days/weeks, depending on when both parties go to settlement). You must save the ALTA Settlement Statement practically for life. The title agent/ title lawyer will go to the courthouse to file the documents associated with the transaction. It can take several weeks/months for the court to record and archive said transaction. Your lender, your realtor, and title company are required to keep records of the transaction for a period of three to five years. The courthouse needs to keep records for decades. However, life happens. No title company, lender or real estate brokerage/Realtor has lasted for life. Lenders sell loan portfolios all the time, usually within months of going to settlement. Banks merge with other lending institutions, which may cause a lender not to stay in place. However, the loan files the lender worked on may remain with the institution. Title companies, and real estate brokerages/Realtors, as lenders may merge with other institutions, or they may close. Mergers, closings, or software updates may disrupt file tracking. The real estate market crash of 2007/2008 brought about many of these mergers and closures, leaving many homeowners with limited or no records of their transactions.

For the reasons mentioned above and for many others such as war, natural disasters, you must preserve a copy of the ratified ALTA Settlement Statement in your records. The ratified ALTA Settlement Statement can serve to PROVE you have sold a property, as well as bought one. The ALTA Settlement Statement is also issued when you refinance a home. When you refinance and pay off a loan, you also get a Disclosure of Release. The Release document is also critical. You need to save all ALTA Settlement Statements and all letters of loan releases. Should you ever sell your property, and the court has a claim of an outstanding loan, the ALTA Settlement Statement and, more importantly, the Disclosure of Release can save your neck from unnecessary financial burden and stress.

You work too hard to achieve the coveted American Dream of homeownership; don’t let a careless mistake cost you your peace of mind and be a financial burden.

#alta #altasettlementstatement #hud1 #settlement #americandream #homeownership #closingdisclosure #mortgage #disclosureofrelease #courtrelease #realestatereview #yearinreview #family #friends #support #familysupport #loyalclients #clientsupport #texasstorm #texaswinterstorm #petrescue #puppies #newbeginnings #newopportunities #leadershipinstitute #nvar #committment #gratitude #preparation #realestatescience #hotmarket #hotsellersmarket #financialportfolio # finances #taxes #homeseller #negotiations #negotingcontracts #beginthehomejourney #homejourney #luisasellsva #home #remax #realtor #remaxhustle #homebuying #homeselling #selling #buying #investing #realestateinvestment #leasing #topproducer ##realtorlife #property #singlefamilyhouse #townhouses #th #sfh #condo #condos t #remaxexecutives #financialstability #financialfreedom #homesweethome #community #neighborhood #pieceofthepie #theamericandream #househunting #homeowner #refinancing #refinace #homerenovation #houserenovation #mortgage #homeownership #newhome #forsale #forlease #nar #sold #homebuyer